The bad:

The Medicaid expansion is eliminated: childless nonpregnant adults no longer covered no matter how poor they are — which would be fine if there were other mechanisms to provide for their healthcare, but it’s basically status quo ante. And, yes, studies have shown that adding people to Medicaid was not actually life-saving (controlled studies from certain pre-O’care pilots in which childless adults were randomly chosen to receive government benefits, and the winners and losers of this lottery were evaluated for their health outcomes) but it did provide for their overall well-being.

(Incidentally, they also replace the existing cost-sharing mechanisms with per-capita allottments; is that “good” or “bad”? I haven’t yet formed an opinion.)

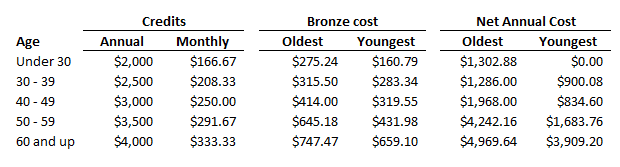

The bill replaces exchange subsidies with flat credits, which I would agree with in principle, but highly dependent on the amount of the credits, and, so far as I can tell, they are quite inadequate.

Here’s a simple analysis based on information from ehealthinsurance.com, using my own zip code (suburban Chicago), and the cheapest possible cost plan, with a $7,100 deductible. You can try this with your own area — perhaps the regional variations are substantial enough that these credits buy more elsewhere.

In the first place, the age-based scale is quite insufficient to make up for the higher costs at older ages, and this’ll only increase when the 3:1 differential is removed. And these are credits per individual, so, naturally, a couple will have double the credits, but also double the shortfall between credits and actual cost. In addition, so far as I can tell, there is no mechanism in the bill for increasing these credits with inflation.

And these credits might be adequate for someone who is self-employed but with a middle-level income. But for the low-income folk, for whom, prior to Medicaid or the subsidies, health insurance was a luxury good? In what world are these credits sufficient? I suppose, in principle, they could (presuming out-of-pocket limits are removed) buy a plan with, instead of a $7,100 deductible, something twice that, but when you’re talking about such a high deductible level, it’s hard to make the case that the remaining value is still worth the logistical trouble of securing health insurance. And if you are planning to give very low income folk catastrophic coverage, then this should be accompanied by a much greater effort at providing access to sliding-scale clinics, which I haven’t seen here or in any other discussion, except for vague statements about grants to states.

(Update: here’s a cool interactive map showing winners and losers by region. Did Kaiser have this in their back pocket to drop numbers in and take live as soon as the plan was released?)

Here’s the bottom line:

Obamacare created new facts on the ground. The GOP might wish that it hadn’t, they might wish that so-called non-profit hospitals would solve the problem by providing true charity care rather than use their funds to build more and fancier wings, might wish that the moderate and middle-income folk without employer-provided health insurance would just perceive of it as a necessary part of their budget and cut other household expenses instead, might wish for all manner of things to happen that don’t. But that’s not where we are. There is a broad consensus that the federal government should, in a meaningful way, provide health insurance to those for whom it is outright impossible to pay for it or for whom its purchase would cause a significant drop in living standards. And the GOP can’t undo that consensus, even if many Republican congressmen dislike it.