I’ve read most of it. All the analyses about the AHCA (“Trumpcare” or “Ryancare”), the proposed GOP replacement for the Affordable Care Act (“Obamacare”) have taken residence in my brain. I’ve also logged countless hours in conversation with an expert in the insurance world.

So now I now offer a quick, admittedly simplistic summary for the non-insurance professional, coupled with suggestions for the church’s response.

Insurance company basics

Insurance companies, health, life, auto, home, etc., are for-profit entities. In our capitalistic economy, it means that they exist to create profits for their shareholders. That’s their business.

For-profit insurers may not be the best way to pay for health care, but that’s not the point. This is what we have.

Reputable insurance companies create good products. Independent agents sell these products earning their living totally by commissions from their sales. Insurance companies manage the funds paid in so there are adequate reserves to pay claims, some of which can run well into the millions.

State laws require insurance companies to keep significant reserve funds on hand to pay claims as they come in. State regulations also require insurers to pay out a certain percentage of their policy revenues each year. It is a highly regulated business.

The management of these vast sums means that insurance companies hold investments in myriad other companies, both in the US and around the world. Insurance companies and the banking system, another for-profit industry, are very entangled with each other.

Because insurance companies are pretty consistently profitable, many pension funds hold massive investments in them. A move to nationalize the insurance industry, i.e., go to a “single-payer” option, would play havoc with those retirement funds.

Insurance=shared risk

Insurance is also a shared-risk business. By its very nature, most people who purchase insurance will not need it, or if they do, will use less than they paid in.

No one likes buying it until they need it. But when they need it, it is a godsend. The nature of health-care pricing in the US makes it scarily risky to be without health insurance. Unfortunately, because of the high cost of medical care in the US, one medical emergency can tip a family firmly into bankruptcy or at the least into on-going financial fragility.

State insurance commissioners regulate insurers rate increases. Insurers must set their rates over a year in advance. The rates fluctuate depending upon the anticipated sales and claims.

Inaccurate predictions can and have brought massively well-capitalized companies down. Everyone gets hurt when that happens. All insurers base their premiums on formulas that rely on the fact that most policy holders will not make a claim in a given year.

If the balance of policy holders swings heavily in the direction of those who will be more likely to make claims, rates must go up or no one will have their claims paid.

Socialist systems vs capitalistic systems

In socialist economies, governments cover health care costs. This is the so-called “single payer system.” Those countries fund health care services by levying high taxes on wage-earners, often as much as 50%.

However, many who live in countries with socialized medicine plans also carry private insurance because it can be difficult to access elective procedures, like knee and hip replacements, otherwise.

In a capitalistic economy which predominates in the United States, private insurers cover a large percentage of health care costs, with exceptions I will mention below. Funds come from the above-explained shared risk principle. Most current health insurance plans have nearly unlimited ceilings for life-time costs.

The US government, under Medicaid, does up the costs for the extremely poor. However, their reimbursement rates are so low that many health care providers won’t take Medicaid patients, effectively rationing their care.

The US also covers the VA health care system. It is not working well.

Now, about Medicare, often held up as a model to use. Many are unaware that those on Medicare who opted to enroll in Medicare Advantage programs use private insurers to pay their claims, not the US government. Thus, those under Medicare Advantage programs have restricted access to various providers, but the programs are fairly cost-effective as the private sector has major motivations to keep costs under control. In a sense, their health care also is rationed.

Retirees who opted for the more expensive Medicare/Medigap programs have no restrictions, no rationing. They pay far more. The government, the “single-payer” remains fully liable for those payments. These are costs that are spiraling out of control and problematic for the national debt.

The ACA and its current fragility

Before the ACA, health insurers (remember, they are for-profit companies) could and did decline to insure those whose coverage would inevitably be very, very expensive, i.e., the older and those with pre-existing conditions.

Since the ACA insisted that insurers not discriminate against those people, the only way it could work was to also insist that the young and healthy become a part of it. Remember: the ACA did not create insurance companies: it used the for-profit ones already in place.

What happened? Because of the lack of restrictions on pre-existing conditions and because the tax penalties were not high enough to force enrollment, often people would wait until some horrific disease was diagnosed and then enroll in an ACA insurance plan.

Insurance companies would pay out thousands to cover medical bills, but the newly insured might pay in only several hundred dollars in premiums. Often, once cared for, those newly insured would then drop out and thus not contribute to the shared risk pool of funds available to pay claims.

Insurance companies, again responsible to their stockholders, began to both raise rates and to bail out of certain markets. More will do so in the future. That much is inevitable.

In the short run, the ACA has been a profound success. More have insurance than ever before. However, its long-term success is questionable. As noted, insurers are pulling out because there is an inadequate pool of healthy, younger people to share the risk.

In addition, for some reason, the previous administration also decreed in 2016 that agents would no longer be paid a commission when selling ACA products, effectively eliminating their income and/or any incentive to sell ACA products.

Clearly, current structure is not sustainable in the long run.

We face a very messy situation. There are no simple answers or quick and easy fixes.

The proposed GOP replacement

Underlying the ACHA (i.e., “Trumpcare”) proposal is the principle of individual freedoms: no one should be mandated to purchase insurance if they don’t want it. Let the free market regulate the rates.

That’s what we had before the ACA. That’s why older people and people with pre-existing conditions were denied coverage in the individual market, although they often could still get in under large group plans. Naturally, employers offering those group plans as part of benefit packages would seek to refrain from hiring those whose health issues might raise their plan prices.

Since the GOP doesn’t want to go on record as denying people health insurance completely, insurers will still be required to accept everyone.

However, they can charge the rates necessary for those otherwise considered uninsurable.

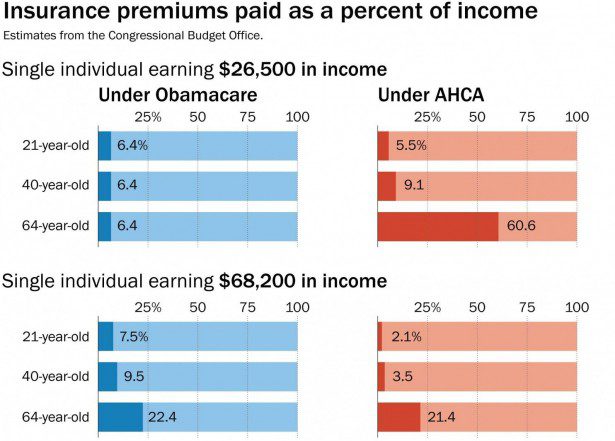

Thus older and generally sicker Americans may need to pay up to 60% of their income for insurance under Trumpcare. Nonetheless, the GOP will keep a promise: everyone technically has “access.” They just can’t afford it.

Unregulated capitalism=survival of the fittest

What we have, then, is a “survival of the fittest” society. It’s what capitalism does. President Obama unquestionably took the country in a socialist, and kinder, direction by his signature achievement.

He also flamed a fire under the libertarians and the conservatives who stand firmly on the idea of encouraging free markets as the guiding principle underlying political decisions.

What does the church do?

The US church tends to operate as capitalists, i.e., the big eat the small, the most social-media adept rise to the top.

However religion as Jesus taught it is inherently socialist, i.e., the last shall become first, everyone shares with everyone else.

The church growth movement rewards an entrepreneurial, competitive, “survival of the fittest” mindset. This competitive mindset can and often does produce huge churches. In both subtle and obvious ways this mindset supports the GOP plan.

It’s just not very Jesus-like.

In addition, it likely that churches will be called on to fill the gaps in our health care system.

Here are some options.

First, let’s look at options within the church.

Remember, our spiritual health and vitality intertwine with our physical health and vitality. Start with aggressively promoting health within church communities. Instead of Bible studies, take a year and gather everyone for a study of Gary Taubes latest book, The Case Against Sugar. Here’s a fairly comprehensive review of the book. I suspect that if we’d all cut our sugar ingestion by 2/3, many of the costly diseases of civilization would simply disappear.

Intentionally go small. Recognize that real disciple-making activity is far more a one-on-one process than large and expensive buildings and state-of-the-art worship teams. We need intensive accountability.

Sit down with any health professionals in your congregations and ask for their ideas to improve community health.

Second, let’s look at political options.

Using respectful dialogue, request your elected representatives to consider the necessary modifications to the ACA so that it will hold together for the next five to ten years while more creative and cost-effective structures can be designed and implemented. The entire nation suffers when we have a chronically ill and uncared-for population

Request as well that Planned Parenthood retain its funding. Remember, no federal funds are used for abortion procedures. But without adequate access to women’s health providers and birth control, we will face a nation of babies born from inadequate uterine environments, virtually guaranteeing an unhealthy childhood, learning disabilities, massive medical needs and early deaths.

Finally, ask your legislative representatives to insist on programs for free and universal child-care. The poorest of our poor children need the best options available, both mentally and physically, in order to develop into healthy, functioning adults.

If we can marry the best of capitalistic energy and socialistic humaneness, we have the basis for a nation to continue to go foward.

If you’ve got other suggestions, please leave them in the comments section below. We can help deal with the growing crisis of inadquate health care in the US.