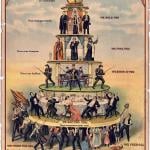

So says Charles Morris, who points out that the current palliatives are trying to get us back to what caused the problem in the first place; namely, too much lending and borrowing:

All these frenzied attempts at staving off recession seem to be aimed merely at jump-starting the consumer borrowing-spending binge that underpinned the ersatz growth of the 2000s. But the real need is to shift to a more balanced system that’s less addicted to high-leverage finance.

Pouring money from the Fed into the banks just delays the day when banks — and now we taxpayers — will have to tally up our losses. The Fed is exchanging Treasury bonds for bundles of subprime mortgages at 98 cents on the dollar. But in the real world, those bundles could barely fetch 30 to 50 cents on the dollar. Does the Fed seriously believe that subprime mortgages are going to recover their value? The Japanese tried papering over bad assets during their 1990s credit crunch, and their economy has barely budged in 20 years.