What’s all this talk about the “yield curve” and why does it matter to you?

The yield curve is a plot line, just like any plot line you would make in a spreadsheet on your computer. It is based on length of time a bond has before it pays out the interest it has promised to pay the person who bought the bond, combined with the price the bond is worth in the open market.

“Short-term” bonds pay out sooner than “long term” bonds. Since economic conditions change as time passes, there is a “risk” involved in buying a long-term bond that the inevitable change in conditions over, say, the next 20 years, will make the interest the buyer on the bond was promised less appealing at the end of that time than it was at the beginning.

For this reason, short-term bonds are considered less “risky” than long-term bonds. That means the people who issue the bonds don’t have to pay as much interest to lure buyers to their short term bonds as they do to their long-term bonds.

Some bonds can be bought and sold on the open market. The price they get when they are bought and sold is part of what we call the bond’s “yield.” The simplest version of yield is just the amount the bond pays (coupon) divided by the price someone pays for the bond when it is traded. Under normal conditions, long-term bonds have a higher yield than short-term bonds.

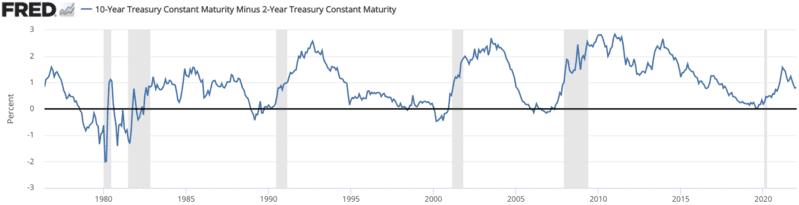

United States Treasury bonds are the standard in the bond market. The “yield curve” is a plot line somebody made that shows the yield of Treasury bonds over time on a line. There are yield curves for short term bonds and yield curves for longer terms bonds. So you have a yield curve for bonds with maturities up to 24 months and others for maturities of 10 years and 20 years.

Normally, the yield curve for long-term bonds are higher than those for short-term bonds.

When the yield curve “inverts” the yield curve for long-term bonds becomes lower than the yield curve for short-term bonds. There are two ways this can happen. Either the yield curve for short-term bonds can go up higher than the yield curve for long term bonds, or the yield curve for long-term bonds can drop lower than that for short term bonds.

All this week, the short-term bond yield curve has been punching up through the long-term bond curve. What that means is that the yields on 24 month treasuries are higher than the yields on 10 and 20 year treasuries. What that means is that bonds are reflecting a kind of investor panic as investors buy up short term bonds. What that means, in simple terms, is that the market is running to safety because the collective wisdom of the market is that things are going to get dicey.

In simpler, less touchy-feely terms, bonds are rocking and rolling. The steady-eddy portion of people’s portfolios is losing money, if not quite like stocks in a down market, not too far off.

That’s kinda scary.

Market history shows that when the yield curve “inverts,” it often signifies that a recession is in the offing. This is even more likely when the curve “inverts” because the short-term curve punched through the long-term curve, which means that people are buying short term bonds and selling long term bonds in expectation of trouble.

However — and this is a big however — many times in the past the yield curve has inverted and … nothing much happened. There was no recession, no stagflation, no Old Testament stuff at all. Sometimes, investors are buying short-term bonds the way consumers bought toilet paper early in the pandemic, because they’re running scared and being silly.

This is all statistics, based on buying trends in the bond market. It’s not a magic formula, and it’s not complicated and arcane. It reflects purchases driving price. All the talk about yield curve inversion is just talk about observed likelihood based on observations of how events sometimes played out in the past.

We are in uncharted history right now. First, we’re trying to pull out of a worldwide pandemic that has killed over a million Americans in a less than two years. The federal government piled on to save us from what would almost certainly have been an economic cataclysm by pumping money into the economy, big time.

The feds dropped interest rates to zero, they handed out money to businesses and regular citizens, and they bought their own bonds. They did all this while the productivity of the overall economy sat at idle, just trying to keep the engines tuned so it could swing back alive when the worst of the pandemic passed.

That my friends is a classic recipe for inflation. If the feds had sat down and thought “how can we cause inflation; let’s go do it” they couldn’t have done any better.

I’m not bashing the government for doing what it had to do to save us from a debacle that would have been a worldwide catastrophe. They had to do it. And it worked. The government saved a lot of lives with their efforts in vaccination and closures, and they saved us from economic freefall with their interventions in the economy.

But everything comes with a price, and we’re paying the inflationary price now.

Now, let’s circle back to the yield curve that has been rattling America’s economic cages these past few days. The yield curve for short term bonds has broken through the yield curve for long term bonds repeatedly. That’s ominous. It says that things are getting dicey.

Whether or not the economics of our time results in a recession is still to be seen. It might. It could get ugly. The fed’s plan to raise interest rates to stamp down inflation is sending the market into a tizzy because we’re dancing on the edge of stagflation.

But a lot of smart people know this and are doing what they can to keep things chill. It could get ugly. But it might not. We’re in for chop in the markets, and bonds are going to rock, but we might just cycle through this and go on.

This particular set of circumstances has never happened before. I can’t tell you if the yield curve dealio is a harbinger or a blip. All I know for sure is that it’s not smart to bet against the United States of America.